Our joint collaboration with the Einstein Telescope program is now resulting into another live deliverable. We have recently finished a high-frequency trading algorithm that works well, is properly tested and that we are putting live now on our own trading account. The results of 1,5 years of hard work and cooperation between the Boosting Alpha team and a team from the University of Maastricht Data Science faculty.

In gravitational wave (GW) detection, signals from multiple GW detectors around the world (Europe, US, Japan) are used. GW signals travel with the speed of light so an “event” from space is never detected at exactly the same timestamp at these detectors. If a signal is detected on all GW detectors, the confidence level is also much higher then when a signal is only detected on 1 GW detector (then it probably is local “noise”).

Our team started with building the whole infrastructure for this project. So initially we build a real-time data collection system that receives streaming data from multiple trading exchanges. We collect every single tick (trade) and every single change to the orderbook. We are talking about collecting and storing massive amounts of data.

Then we set ourselves two challenges:

1 – Can we find market inefficiencies (situations where prices for the same assets are different on different exchanges) and benefit from this? Taking into account trading fees, slippage, trading risk etcetera.

2 – Can we somehow combine the datasets from different exchanges into a new dataset that has higher-accuracy and less noise (can we increase the confidence level)?

The trading algorithm that we put live now is based on challenge 1. We are still working on finalizing the model for challenge 2. That model might actually become useful in GW detection as well since currently every GW telescope has its own calculation pipeline and with a form of “majority voting” the results from the individual telescopes are combined into a final decision.

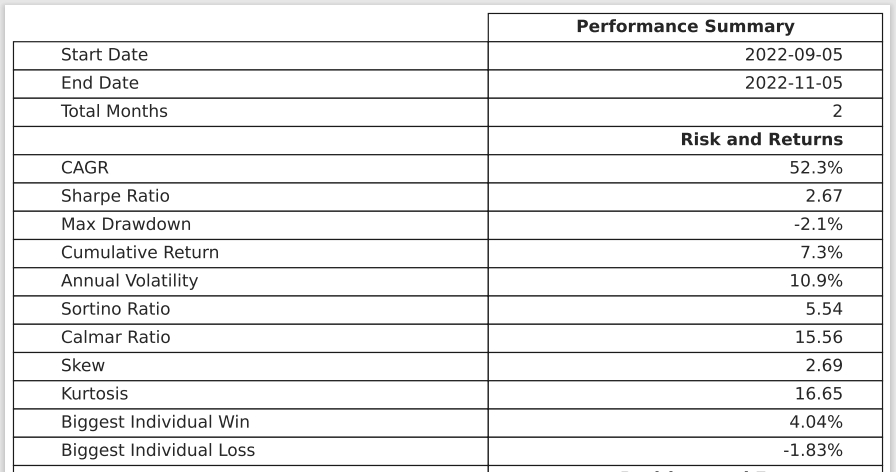

We currently estimate that our new trading algorithm can roughly generate about 50% return annually but with a very low max drawdown and risk level. This is obviously because it is based on short-term market inefficiencies. The average trade position is only open for about 20 seconds. At the moment the model only runs on some big-name coins, but we can obviously easily expand it to multiple coins and multiple financial markets later.

The only issue is the huge amount of data. Running historical backtests takes ages and big Compute power. Luckily, we already have a lot of experience with this type of stuff and we have the hardware, knowledge and infrastructure to actually do it properly. High-frequency trading is usually the domain of very capital-intensive big-name hedge funds / market makers. The capability to accurately enter and exit trading positions in a matter of seconds obviously also requires a lot of infrastructure.

#boostingalpha #einsteintelescope #quant #artificialintelligence